Fixed vs. Variable Energy Tariffs for Accountancy Companies: Which is Best?

For most accountancy firms, a fixed-rate energy tariff is the smarter and safer choice — and the numbers back it up.

Running an accountancy practice means managing client deadlines, compliance requirements, and tight overhead budgets all at once. Energy bills might not be the first cost that comes to mind — but choosing the wrong tariff can quietly chip away at your profit margins every single month. Understanding the difference between fixed and variable energy tariffs is one of the simplest ways to bring more certainty to your operating costs.

The Two Main Energy Tariff Types — Explained Simply

Fixed-Rate Tariff

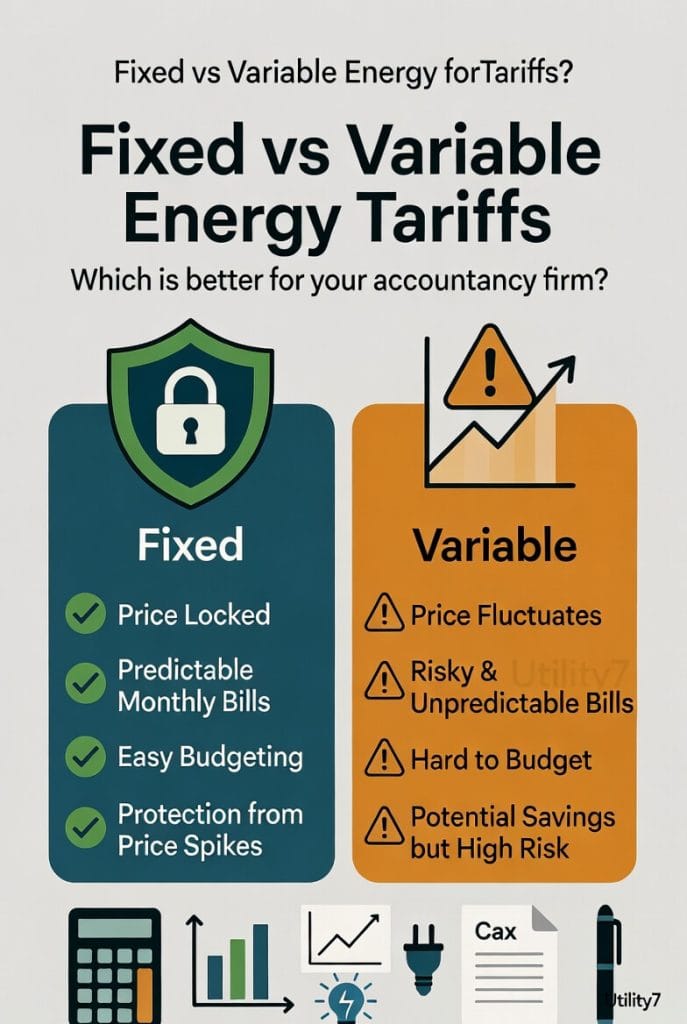

With a fixed-rate tariff, the price you pay per unit of energy (kWh) is locked in for the duration of your contract — typically 12, 24, or 36 months. Your bill may still vary slightly depending on how much energy you consume, but the unit rate itself won’t change regardless of what’s happening in the wider energy market. No surprises. No sudden spikes. Just consistent pricing you can plan around.

Variable-Rate Tariff

A variable-rate tariff moves in line with the wholesale energy market. Prices can rise or fall — sometimes with very little notice. When energy prices drop, you could benefit from lower bills. But when prices spike, as they have done dramatically in recent years, your costs can increase significantly and without warning.

Fixed vs. Variable Energy Tariffs for Accountancy Companies: Side-by-Side Comparison

| Feature | Fixed-Rate Tariff | Variable-Rate Tariff |

|---|---|---|

| Price Stability | Locked in for contract term | Changes with the market |

| Budget Planning | Easy — predictable monthly cost | Difficult — bills can vary widely |

| Market Savings | Not available | Possible when prices drop |

| Exit Fees | Usually applies | Often none |

| Best For | Stability-focused firms | Risk-tolerant, active switchers |

Why Fixed-Rate Tariffs Suit Most Accountancy Firms

1. Predictable Costs = Better Budgeting

Accountancy firms carry consistent monthly overheads — staff salaries, software licences, office rent. Adding unpredictable energy bills into that mix creates unnecessary complexity. A fixed tariff lets you include a set energy cost in your monthly budget with complete confidence, keeping your P&L clean and your forecasts accurate.

2. Protection From Market Volatility

The wholesale energy market is notoriously volatile. Geopolitical events, seasonal demand, and supply disruptions can cause prices to spike rapidly. A fixed-rate contract insulates your firm from these external shocks — meaning your bottom line stays protected even when the wider market turns against you.

3. Focus on Growing Your Practice

Constantly monitoring energy prices and switching suppliers to chase lower variable rates takes time you simply don’t have. A fixed tariff removes that distraction entirely, freeing you to focus on what actually drives revenue — your clients, your team, and your services.

4. Easier Financial Planning for Investment

Whether you’re planning to upgrade your server infrastructure, expand your office space, or invest in new audit software, knowing your fixed overheads makes financial forecasting far more reliable. It also makes your own accounts more presentable — something every accountant should appreciate.

When a Variable Tariff Might Still Be Worth Considering

Variable tariffs aren’t always the wrong call. If wholesale energy prices are currently high and forecasted to fall significantly, locking into a fixed deal could mean overpaying relative to where the market moves. However, predicting energy markets is notoriously difficult — even professional analysts get it wrong regularly.

Variable tariffs can also suit firms in transition — if you’re planning to move offices, merge with another practice, or downsize in the near term and don’t want to be tied into a long contract. Just ensure you’re actively monitoring prices and ready to act quickly if costs rise.

Practical Steps to Choose the Right Tariff

- Review your last 3–6 months of energy bills to understand your typical usage patterns.

- Identify how much of your consumption is driven by servers, workstations, climate control, and lighting.

- Compare multiple suppliers — don’t assume your current provider is still offering the best deal.

- Pay close attention to contract length, unit rates, standing charges, and any exit fees.

- Ask about green energy options if sustainability matters to your firm’s brand.

- Set a calendar reminder before your contract ends so you can reassess and switch before rolling onto a more expensive out-of-contract rate.

Key Energy Tips Specific to Accountancy Offices

Servers & IT Infrastructure: Servers running 24/7 are one of your biggest energy draws. Upgrading to energy-efficient hardware or cloud-based solutions can meaningfully reduce consumption over time.

Workstations & Monitors: Enabling power-saving modes on computers and monitors during idle periods is a simple step that adds up across a full office.

Climate Control: Heating and cooling a professional client-facing environment is non-negotiable — but a programmable thermostat ensures you’re not paying to heat an empty office over weekends.

Lighting: Switching to LED lighting and installing motion sensors in low-traffic areas like meeting rooms and corridors is a low-cost upgrade with a fast payback period.

Final Thoughts

For most financial professionals, choosing between fixed vs. variable energy tariffs for accountancy companies comes down to one thing: how much uncertainty can your overhead budget comfortably absorb? While variable tariffs can occasionally deliver short-term savings, the risk of sudden price rises makes them a less reliable foundation for a business where precision and predictability are everything.

The smartest move is to stay proactive — compare deals regularly, understand your usage, and always switch before your contract rolls over to a default rate.

Ready to find a better energy deal for your accountancy firm?

Visit Utility7 at www.utility7.com to compare energy tariffs tailored for professional services businesses. It only takes a few minutes to find out if you could be saving — and in a profession built on numbers, every saving counts.